RESULTS FOR THE YEAR ENDED 31 DECEMBER 2023

27 February 2024

RECORD EARNINGS, STRONG OUTLOOK FOR 2024/25 AND SIGNIFICANT GROWTH OPPORTUNITIES

Joe Lister, Chief Executive of Unite Students, commented:

“This is a strong set of results, driven by full occupancy, rental growth and substantial investment into our platform and portfolio. Our pipeline of developments, asset management projects and our new university partnership present a substantial growth opportunity for the business.

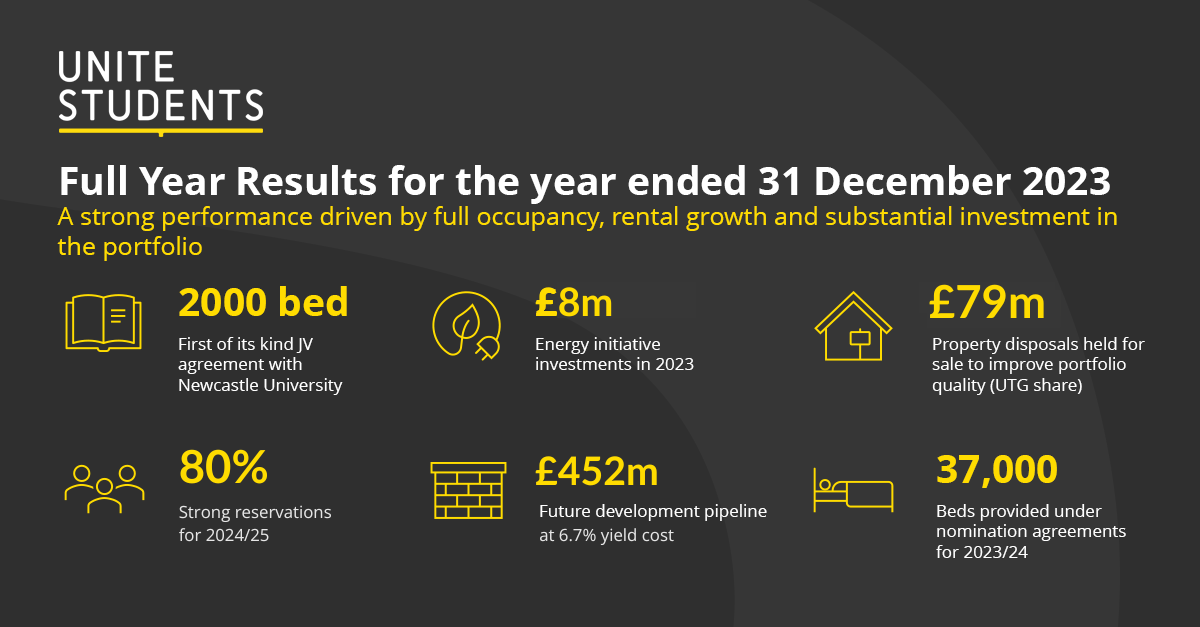

“The supply-demand imbalance of student accommodation is acute and continues to intensify. We play a leading role in tackling this shortage, easing pressure on the wider housing market and freeing up homes for families. Our development and asset management pipeline stands at a record £1.3 billion and we are taking an innovative approach to delivering more homes for students. University partnerships provide a compelling opportunity to deliver new, high-quality accommodation and our first joint venture with Newcastle University is only possible for a business of our reputation, scale and development expertise.

“We are trusted by students, parents and universities to deliver high-quality, safe and affordable accommodation where it is needed the most. Our strong leasing performance supports continued earnings growth in 2024 and we are confident that our all-inclusive offer, student support programmes and balanced approach to rental increases will continue to provide real value for money.”

| Year ended | 31 December 2023 | 31 December 2022 | Change |

| Adjusted earnings1,3 | £184.3m | £163.4m | 13% |

| Adjusted EPS1,3 | 44.3p | 40.9p | 8% |

| IFRS profit before tax | £102.5m | £350.5m | (71)% |

| IFRS diluted EPS | 24.6p | 87.6p | (72)% |

| Dividend per share | 35.4p | 32.7p | 8% |

| Total accounting return1 | 2.9% | 8.1% | |

| As at | 31 December 2023 | 31 December 2022 | Change |

| EPRA NTA per share1 | 920p | 927p | (1%) |

| IFRS net assets per share | 931p | 944p | (1%) |

| Net debt: EBITDA | 6.1x | 7.3x | (1.2x) |

| Loan to value2 | 28% | 31% | (3)ppts |

HIGHLIGHTS

Full occupancy in 2023/24, strong demand for 2024/25

- 8% occupancy and 7.4% rental growth for the 2023/24 academic year (2022/23: 99.3% and 3.5%)

- Strong reservations for 2024/25 80% (2023/24: 83%)

- 3p adjusted EPS in 2023, +8% YoY (2022: 40.9p)

Sustained earnings growth from our best-in-class platform

- Confident in delivering rental growth of at least 6% for 2024/25 (previously at least 5%)

- Guidance for 3-5% growth in adjusted EPS in 2024 to 45.5-46.5p

- Targeting 10-12% Total Accounting Return (TAR) in 2024, before yield movement

- Earnings growth to accelerate from 2026 as development completions increase

- £26 million technology upgrade to enhance customer experience and EBIT margins from 2025

Housing supply unable to meet student demand

- Significant need for high-quality, affordable student homes

- New PBSA supply 60% below pre-pandemic levels and over 100,000 reduction in HMO beds available

Investment activity aligned to the strongest universities

- Delivery of £60 million Morriss House development in Nottingham at 8.5% yield on cost

- Rental portfolio enhanced through £24 million of refurbishments at a 9% yield on cost

- £197 million of disposals held for sale to improve portfolio quality (Unite share: £79 million)

Record £1.3 billion development pipeline in the strongest markets

- £569 million committed pipeline in Russell Group cities at 6.5% yield on cost

- £250 million joint venture agreed with Newcastle University announced in February

- Future development pipeline of £452 million at 6.7% yield on cost in cities with tightest supply

- New London scheme added to future pipeline for delivery in 2028

- Targeting £50-75 million p.a. of refurbishment projects at 8%+ yield on cost

Strong balance sheet underpinned by resilient valuations

- £5,510 million portfolio valuation (Unite share), up 1.2% on a like-for-like basis (2022: £5,397 million)

- 4% rental growth offsetting 31bps yield expansion

- TAR of 2.9% (2022: 8.1%), reflecting 1% reduction in NTA to 920p (2022: 927p)

- Continued investment in fire safety, resulting in 9p of new commitments net of claims

- Net debt: EBITDA reduced to 6.1x (2022: 7.3x), with LTV of 28% (2022: 31%)

Delivering on sustainability targets

- Significant improvement in EPC ratings, over 99% of portfolio now A-C rated (2022: 80%)

-

The financial statements are prepared in accordance with International Financial Reporting Standards (IFRS). These financial highlights are based on the European Public Real Estate Association (EPRA) best practice recommendations and these performance measures are published as they are intended to help users in the comparability of these results across other listed real estate companies in Europe. The metrics are also used internally to measure and manage the business and to align to the performance related conditions for Directors’ remuneration. See glossary for definitions.

-

Excludes IFRS 16 related balances recognised in respect of leased properties. See glossary for definitions.

-

Adjusted earnings and adjusted EPS remove the impact of SaaS implementation costs and abortive acquisition costs from EPRA earnings and EPRA EPS. See glossary for definitions and note 7 for calculations and reconciliations.

For further information, please contact:

Unite Students

Joe Lister / Mike Burt / Saxon Ridley Tel: +44 117 302 7005

Unite press office Tel: +44 117 450 6300

Powerscourt

Justin Griffiths / Victoria Heslop Tel: +44 20 7250 1446

{kind=link}